NYC Hotel Tax Exemption for Business: 2026 Guide

Disclosure: This post may contain affiliate links. We may earn a commission for purchases made through links in this post, at no cost to you.

NYC hotel tax exemption for business stays is defined as a legal reduction or elimination of the 5.875% Hotel Room Occupancy Tax (HROT) applied to qualifying guests, most commonly those staying 30 or more consecutive nights or those holding valid exemption documentation from the NYC Department of Finance. Business owners and event planners who understand these rules can avoid paying a combined lodging tax burden of approximately 14.75% plus flat per-room fees on qualifying stays. The nyc hotel tax exemption business explained correctly is not a blanket benefit. It requires precise timing, the right paperwork, and a clear understanding of which tax layers are actually waivable.

What taxes make up the NYC hotel tax for business lodging?

NYC hotel stays carry four separate tax components, and most business owners are surprised to learn that exemptions only apply to one of them. The full NYC hotel tax structure breaks down as follows:

| Tax Component | Rate |

|---|---|

| New York State sales tax | 4% |

| NYC sales tax | 4.5% |

| Metropolitan Commuter Transportation District (MCTD) surcharge | 0.375% |

| NYC Hotel Room Occupancy Tax (HROT) | 5.875% |

| Flat per-room fee | $1.50 or $2.00 per night |

That combined rate lands at roughly 14.75% before the flat fees. On a $300 per night corporate room, that adds over $44 in taxes per night before any flat charges.

The HROT is the only layer where a business hotel tax exemption typically applies. The New York State sales tax, NYC sales tax, and MCTD surcharge remain in place regardless of your exemption status. This is the detail most business travelers miss. They assume an “exemption” wipes the slate clean, but you are really only removing one slice of a four-layer tax structure.

Understanding hotel fees and tax layering before you book is the only way to build an accurate lodging budget. For event planners managing blocks of rooms across multiple nights, even a partial exemption on the HROT adds up to real savings.

Which business stays qualify for NYC hotel tax exemption?

The clearest and most broadly available NYC lodging tax exemption is the 30-consecutive-night rule. Starting on night 31, the Hotel Room Occupancy Tax no longer applies to the stay. The first 30 nights remain fully taxable, with no exceptions.

This rule matters most for:

- Long-term project teams stationed in NYC for extended corporate assignments

- Event planners booking staff or talent for productions lasting more than a month

- Corporate relocations where employees need temporary housing before signing a lease

- Government contractors on extended federal or city projects

Beyond the 30-night rule, certain entities qualify for exemption regardless of stay length. These include federal and state government employees on official travel, qualifying nonprofit organizations, and some diplomatic personnel. Each of these categories requires valid written documentation provided at the time of booking or check-in. A government ID alone is not enough. You need the correct exemption certificate, issued by the appropriate authority, presented before the hotel processes your payment.

Pro Tip: Request the hotel’s specific exemption certificate form before your arrival date. Some properties use their own internal forms in addition to standard government certificates. Showing up with the wrong paperwork at check-in means you pay the full tax rate, with very limited options to recover it later.

The burden of proof rests on the hotel operator, but the documentation responsibility falls squarely on you as the guest. If you fail to provide the correct paperwork at the right time, the hotel is required to collect the tax. Post-stay refund claims are rarely successful and involve a lengthy process with the NYC Department of Finance.

What compliance challenges and audit risks should business owners know?

Hotel operators in NYC function as tax collectors on behalf of the city. That means the hotel, not the guest, carries the primary legal liability for proper tax collection and remittance. Hotels must file quarterly occupancy tax returns and remit collected taxes on time. Late filings trigger penalties starting at 5% per month. That financial pressure is exactly why front desk staff follow strict documentation policies.

Here is where business owners and event planners run into trouble:

- Assuming verbal confirmation is enough. A hotel employee saying “you’re exempt” at check-in means nothing without a completed certificate on file.

- Submitting incomplete certificates. Missing signatures, wrong tax years, or incorrect entity names invalidate an exemption claim entirely.

- Failing to track exemption stays separately. Mixing exempt and taxable nights in the same invoice creates accounting confusion and audit exposure.

- Ignoring the UBT risk for active lodging operations. Short-term rentals with cleaning, concierge, or guest services are classified as active business operations by NYC tax authorities, which triggers an additional 4% Unincorporated Business Tax (UBT). Pure passive rental ownership avoids UBT, but the line between passive and active is thin.

Pro Tip: Train your travel coordinator or office manager to maintain a dedicated exemption file for every NYC hotel stay. Include a copy of the certificate submitted, the hotel’s acknowledgment, and the final invoice showing the tax adjustment. This file is your first line of defense in any audit.

NYC hotel tax audits focus on proof of exemption and proper tax collection records. When documentation is missing, auditors reconstruct revenue from other records and assess taxes, penalties, and interest on the full amount. The cost of a failed audit far exceeds the cost of getting the paperwork right the first time.

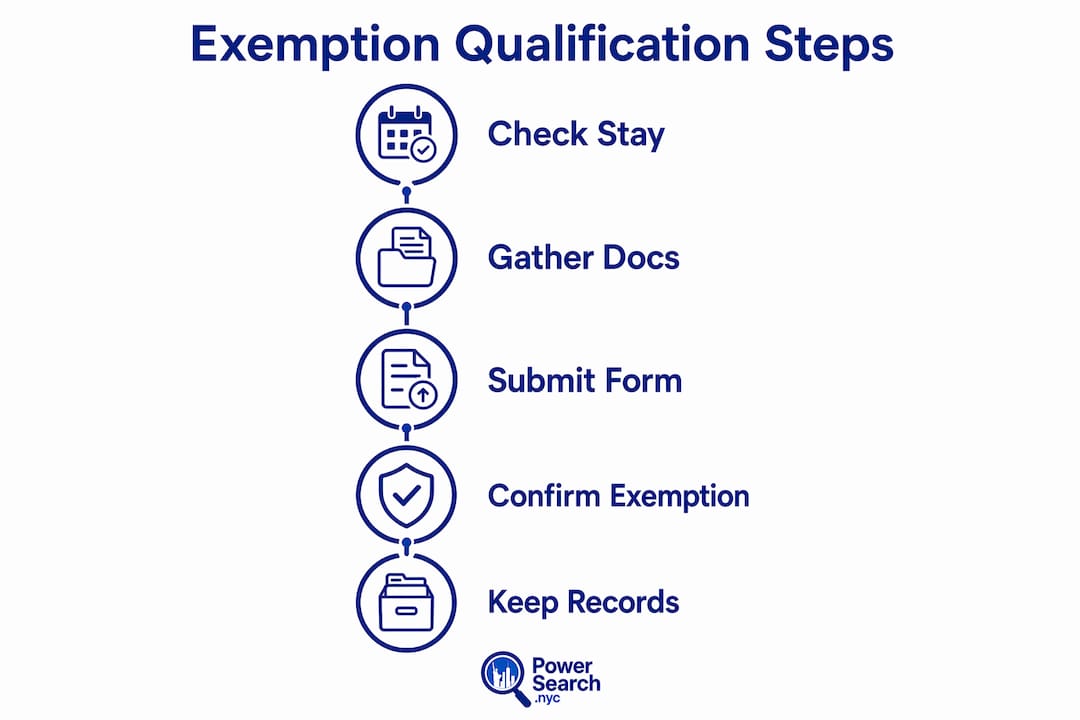

How to manage NYC hotel tax exemptions for corporate travel and events

Practical exemption management starts before you book, not at check-in. Here is a clear process that works for both business owners and event planners:

- Verify eligibility first. Confirm whether your organization, the nature of the stay, or the length of the booking qualifies for any exemption before committing to a property.

- Gather documentation early. Collect government IDs, nonprofit certificates, or other required forms at least one week before arrival. Contact the hotel directly to confirm which documents they accept.

- Communicate with the hotel in writing. Send your exemption documentation by email before check-in. This creates a paper trail and gives the hotel time to flag your reservation correctly in their system.

- Plan for the 30-night threshold strategically. If your event or project runs 35 nights, structure the booking as a single continuous stay rather than two separate reservations. Splitting the stay resets the 30-night clock.

- Use accounting software to track exempt nights. Flag exemption transactions separately in your system so they appear correctly on tax filings and internal reports.

- Review the final invoice before checkout. Confirm that the HROT has been removed for qualifying nights. Errors are far easier to correct before you leave the property.

For event planners booking corporate hotel rates in NYC, understanding the full tax picture also helps during rate negotiations. Hotels sometimes build tax assumptions into their group rate quotes. Knowing your exemption status gives you a factual basis to push back on inflated estimates.

NYC hotel tier classification also affects how properties handle exemption requests. Luxury and full-service hotels typically have dedicated accounting staff who process exemption certificates efficiently. Smaller boutique properties may require more follow-up and clearer communication from your team.

Key Takeaways

NYC hotel tax exemption for business stays requires precise documentation and timing. The 30-night rule and entity-based exemptions only remove the HROT layer, not the full 14.75% combined tax burden.

| Point | Details |

|---|---|

| HROT is the only exempt layer | The 5.875% Hotel Room Occupancy Tax is the only component waivable; state and city sales taxes still apply. |

| 30-night rule starts on night 31 | The first 30 nights are always taxable; exemption triggers automatically from night 31 onward. |

| Documentation must come first | Submit exemption certificates at booking or check-in; post-stay claims are rarely honored. |

| Audit risk is real and costly | Missing documentation leads to reconstructed assessments, penalties starting at 5% per month, and interest charges. |

| Active lodging operations face UBT | Short-term rentals with guest services may trigger an additional 4% Unincorporated Business Tax on top of hotel taxes. |

What I’ve learned from watching businesses get this wrong

I’ve seen business owners walk into NYC hotel stays with total confidence, assuming their nonprofit status or government contract automatically waives the hotel tax. It almost never works that way. The NYC Department of Finance does not operate on assumptions. Neither do hotel front desks.

The most common mistake is treating the exemption as a post-booking fix. Someone realizes mid-stay that they might qualify, asks the front desk, and gets a polite but firm “we need the certificate at check-in.” That’s not the hotel being difficult. That’s the hotel protecting itself from audit liability, which is entirely reasonable given the strict documentation standards they operate under.

What actually works is treating exemption management like a procurement process. You verify eligibility, gather the paperwork, confirm with the hotel in writing, and check the final invoice before you leave. That sequence, done consistently, eliminates most of the risk. The business owners who do this well also tend to negotiate better group rates because they understand the full cost picture, including taxes, flat fees, and any additional parking or service charges that inflate the real cost of a stay.

My honest advice: budget for the full 14.75% tax rate as your baseline. Then work backward from there. Any exemption you successfully claim is a genuine saving, not an assumption.

— Mark

Planning your next NYC business stay with Powersearch

Sorting through NYC hotel options while keeping tax implications in mind is genuinely easier when you have the right search tools. Powersearch is built for exactly this kind of planning, whether you are booking a single executive room or coordinating a multi-week event block.

The NYC hotel search tool on Powersearch lets you filter by neighborhood, price point, and amenity type so you can identify properties that fit your budget after taxes, not before. Business travelers and event planners use it to compare options across Manhattan and the boroughs without wading through irrelevant listings. If you are managing corporate lodging costs in NYC, starting your search on Powersearch puts the full picture in front of you from the first click.

FAQ

What is the NYC hotel tax exemption for businesses?

The NYC hotel tax exemption for businesses is a waiver of the 5.875% Hotel Room Occupancy Tax, available to stays of 30 or more consecutive nights or to qualifying entities like government agencies and nonprofits with valid documentation.

How do I apply for the NYC hotel tax exemption?

Submit the required exemption certificate, such as a government ID or nonprofit certificate, directly to the hotel at the time of booking or check-in. Post-stay claims are rarely accepted, so timing is critical.

Does the exemption remove all NYC hotel taxes?

No. The exemption only removes the 5.875% Hotel Room Occupancy Tax. New York State sales tax (4%), NYC sales tax (4.5%), and the MCTD surcharge (0.375%) still apply to all stays.

What happens if I don’t provide documentation at check-in?

The hotel is required to collect the full tax. Missing documentation results in the tax being charged with very limited options for a refund afterward.

Can short-term rental operators claim the NYC business tax exemption?

Only passive rental owners avoid the Unincorporated Business Tax. Short-term rentals that include cleaning, concierge, or guest services are classified as active business operations and may trigger an additional 4% UBT obligation.

No Comments